Malaysian glove makers poised for recovery as demand increases: HLIB

By CS Ming

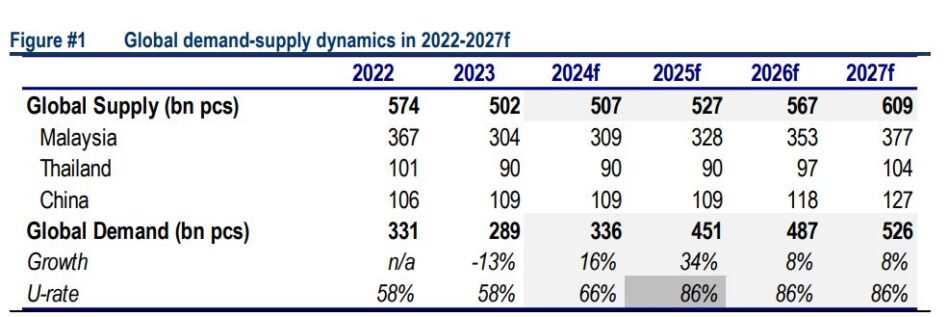

BASED on Hong Leong Investment Bank (HLIB)’s forecast, the global supply-demand dynamics for medical rubber gloves is projected to reach equilibrium by 2025, with global plant utilisation rates improving to 85%, up from 65% in 2024.

This will be driven by customer restocking activities in response to depleting inventories built-up during the Covid-19 pandemic, along with a more rational capacity expansion among regional players.

“Hence, we anticipate sustained recovery momentum in sales volumes for glove makers under our coverage,” said HLIB in the recent Sector Outlook.

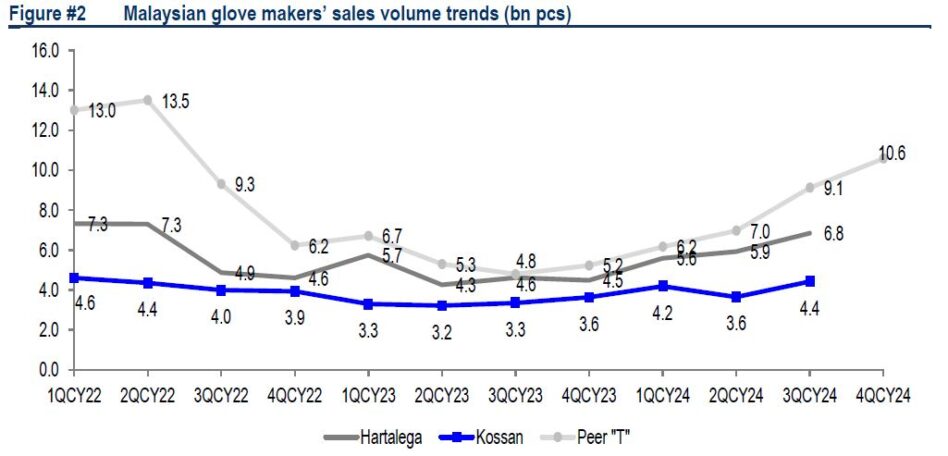

For now, HLIB observed better sales trends among Malaysian players since the bottoming out in quarter two and quarter three of calendar year 2023 (CY23).

Notably, major Chinese glove makers have been operating at full nitrile glove capacity utilisation since 2QCY23.

“Given quality issues associated with Chinese gloves, along with the incremental US tariff increases in 2025 and 2026, we stick by our previous view that the sales volume recovery journey will be asymmetrical,” said HLIB.

If trade is diverted to Malaysia, HLIB believes US medical rubber glove distributors are likely to prioritise:

(i) reputable companies (particularly the listed Big 4) and

(ii) established business relationships (with proven track records and it could take at least three months of qualification procedures for a new business relationship).

Hence, HLIB sees Hartalega and Kossan as clear beneficiaries, given their listing status and having relatively higher exposure to US customers. Also, Hartalega and Kossan have not been served with Withhold Release Order (WRO) by US CBP before.

All in, this trend will benefit most Malaysian players, but it is skewed more towards Hartalega and Kossan.

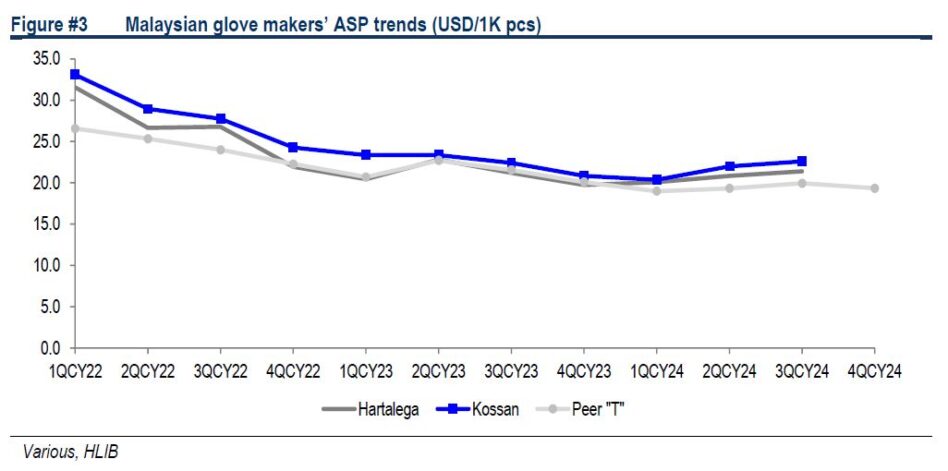

“We believe that average selling prices (ASP) have bottomed out in 1QCY24,” said HLIB.

Also, the cost-pass-through mechanism for both Kossan and Hartalega have been gradually reinstated to 100% by Nov/Dec 2024 respectively.

This was largely underpinned by their strong business relationships with US distributors, which allowed them to capitalise on the “US-premium” pricing mechanism from Oct orders onwards.

In contrast, other listed peers lagged, achieving only a 70% cost passthrough rate in late-2024.

The reinstatement of the mechanism is particularly crucial, amid a volatile forex climate and potential rise in labour costs – planned minimum wage hike, introduction of a multi-tier levy system for foreign labour, along with possible EPF contributions for non-citizen workers in 2025.

Although President-elect Trump has threatened the world with tariffs, HLIB’s view is that Malaysia is not the primary target, given that it is ranked as the 13th largest trade deficit partner (goods only) with the US in 2023.

In any case, should they impose a baseline tariff of 10%-20%, HLIB reckon Malaysian glove manufacturers are still able to pass on this to US glove distributors.

This is because US-made nitrile medical rubber gloves are priced at USD0.01-0.03/pc (or USD10-30/1k pcs) premium to Malaysian-made ones with ASP of USD20-21/1k pcs in Jan 2024; this price difference represents a 49%- 146% premium.

Based on their channel checks, a Chinese glove maker is diversifying their manufacturing facilities to Indonesia to evade the incremental US tariff on Chinese-made medical rubber gloves (taking effect in 2025 and 2026).

However, HLIB believes it is still too early to price in any potential oversupply risks associated with this ‘China + 1’ strategy in Indonesia, primarily due to:

(i) the awareness of the American Medical Manufacturers Association of this geographical diversification.

(ii) uncertainty surrounding Indonesia’s overall operating cost advantages compared to Malaysian competitors, along with the execution risks involved.

Nevertheless, Indonesia presents a new operating landscape for Chinese glove makers, further complicating the potential for large-scale expansion.

“Besides, any new expansion move will take time to roll-out. In our market strategy report dated 17 Dec 2024, we have already revised our outlook for the glove sector by downgrading it to Neutral, following strong share price performance since mid-Sep 2024,” said HLIB.

While HLIB remains optimistic about the improving operating conditions for glove manufacturers, they believe that the recovery thesis for 2025 is already largely priced in.

HLIB only has one Buy rating on Kossan (Target Price: RM3.00) under their coverage, driven primarily by its ongoing PE rerating play.

While we remain optimistic about the improving operating conditions for glove manufacturers, we believe that the recovery thesis for 2025 is already largely priced in.

We only have one Buy rating on Kossan (TP: RM3.00) under our coverage, driven primarily by its ongoing PE rerating play. —Jan 15, 2025

BASED on Hong Leong Investment Bank (HLIB)’s forecast, the global supply-demand dynamics for medical rubber gloves is projected to reach equilibrium by 2025, with global plant utilisation rates improving to 85%, up from 65% in 2024.

This will be driven by customer restocking activities in response to depleting inventories built-up during the Covid-19 pandemic, along with a more rational capacity expansion among regional players.

“Hence, we anticipate sustained recovery momentum in sales volumes for glove makers under our coverage,” said HLIB in the recent Sector Outlook.

For now, HLIB observed better sales trends among Malaysian players since the bottoming out in quarter two and quarter three of calendar year 2023 (CY23).

Notably, major Chinese glove makers have been operating at full nitrile glove capacity utilisation since 2QCY23.

“Given quality issues associated with Chinese gloves, along with the incremental US tariff increases in 2025 and 2026, we stick by our previous view that the sales volume recovery journey will be asymmetrical,” said HLIB.

If trade is diverted to Malaysia, HLIB believes US medical rubber glove distributors are likely to prioritise:

(i) reputable companies (particularly the listed Big 4) and

(ii) established business relationships (with proven track records and it could take at least three months of qualification procedures for a new business relationship).

Hence, HLIB sees Hartalega and Kossan as clear beneficiaries, given their listing status and having relatively higher exposure to US customers. Also, Hartalega and Kossan have not been served with Withhold Release Order (WRO) by US CBP before.

All in, this trend will benefit most Malaysian players, but it is skewed more towards Hartalega and Kossan.

“We believe that average selling prices (ASP) have bottomed out in 1QCY24,” said HLIB.

Also, the cost-pass-through mechanism for both Kossan and Hartalega have been gradually reinstated to 100% by Nov/Dec 2024 respectively.

This was largely underpinned by their strong business relationships with US distributors, which allowed them to capitalise on the “US-premium” pricing mechanism from Oct orders onwards.

In contrast, other listed peers lagged, achieving only a 70% cost passthrough rate in late-2024.

The reinstatement of the mechanism is particularly crucial, amid a volatile forex climate and potential rise in labour costs – planned minimum wage hike, introduction of a multi-tier levy system for foreign labour, along with possible EPF contributions for non-citizen workers in 2025.

Although President-elect Trump has threatened the world with tariffs, HLIB’s view is that Malaysia is not the primary target, given that it is ranked as the 13th largest trade deficit partner (goods only) with the US in 2023.

In any case, should they impose a baseline tariff of 10%-20%, HLIB reckon Malaysian glove manufacturers are still able to pass on this to US glove distributors.

This is because US-made nitrile medical rubber gloves are priced at USD0.01-0.03/pc (or USD10-30/1k pcs) premium to Malaysian-made ones with ASP of USD20-21/1k pcs in Jan 2024; this price difference represents a 49%- 146% premium.

Based on their channel checks, a Chinese glove maker is diversifying their manufacturing facilities to Indonesia to evade the incremental US tariff on Chinese-made medical rubber gloves (taking effect in 2025 and 2026).

However, HLIB believes it is still too early to price in any potential oversupply risks associated with this ‘China + 1’ strategy in Indonesia, primarily due to:

(i) the awareness of the American Medical Manufacturers Association of this geographical diversification.

(ii) uncertainty surrounding Indonesia’s overall operating cost advantages compared to Malaysian competitors, along with the execution risks involved.

Nevertheless, Indonesia presents a new operating landscape for Chinese glove makers, further complicating the potential for large-scale expansion.

“Besides, any new expansion move will take time to roll-out. In our market strategy report dated 17 Dec 2024, we have already revised our outlook for the glove sector by downgrading it to Neutral, following strong share price performance since mid-Sep 2024,” said HLIB.

While HLIB remains optimistic about the improving operating conditions for glove manufacturers, they believe that the recovery thesis for 2025 is already largely priced in.

HLIB only has one Buy rating on Kossan (Target Price: RM3.00) under their coverage, driven primarily by its ongoing PE rerating play.

While we remain optimistic about the improving operating conditions for glove manufacturers, we believe that the recovery thesis for 2025 is already largely priced in.

We only have one Buy rating on Kossan (TP: RM3.00) under our coverage, driven primarily by its ongoing PE rerating play. —Jan 15, 2025

No comments:

Post a Comment