P Gunasegaram

COMMENT | This question was raised during the time of the previous Pakatan Harapan government in 2019 - when then finance minister Lim Guan Eng claimed debt had reached RM1 trillion - but nothing came out of it.

We had occasion to comment upon it here. Why that never took off, we were not told, but I suspect politics and the subsequent Sheraton Move in February 2020.

The event put the focus of the government on continued politicking and delayed indefinitely what needed to be done for the country and the economy.

Now, PKR’s Subang MP, Wong Chen, has raised it anew, suggesting that Petronas should be listed and the money raised used to reduce the national debt and progressively put national finances in a good position.

Let’s examine the issues involved. From a timing point of view, it could not be better for Petronas as the national oil and gas company is poised to make record profits for last year (see chart below).

COMMENT | This question was raised during the time of the previous Pakatan Harapan government in 2019 - when then finance minister Lim Guan Eng claimed debt had reached RM1 trillion - but nothing came out of it.

We had occasion to comment upon it here. Why that never took off, we were not told, but I suspect politics and the subsequent Sheraton Move in February 2020.

The event put the focus of the government on continued politicking and delayed indefinitely what needed to be done for the country and the economy.

Now, PKR’s Subang MP, Wong Chen, has raised it anew, suggesting that Petronas should be listed and the money raised used to reduce the national debt and progressively put national finances in a good position.

Let’s examine the issues involved. From a timing point of view, it could not be better for Petronas as the national oil and gas company is poised to make record profits for last year (see chart below).

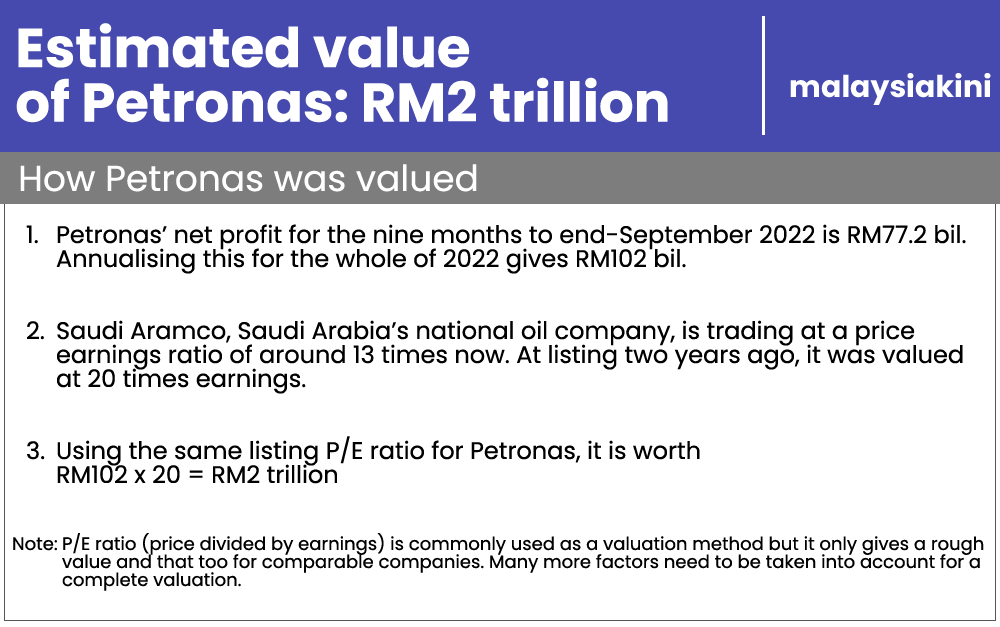

With revenue for the nine months of 2022 (up to Sept 30) already at RM271 billion and profit after tax at RM77 billion, on the back of rising oil prices (see last row in the chart), the full-year revenue is likely to exceed RM360 billion while net profit will exceed RM100 billion.

A very rough valuation is given in the table, which puts a valuation of Petronas at RM2 trillion, using Saudi Arabia’s national oil company, Saudi Aramco, as the benchmark. That’s a fair comparison to make as Aramco is a state-owned company with a similar structure to Petronas in terms of profit share with oil and gas concessionaires.

That is obviously a very high valuation. Even if a P/E of 15 times is used, the value is still about RM1.5 trillion. So the valuation range for Petronas could be about as high as the entire value of the Malaysian market of about RM1.8 trillion!

Petronas, therefore, cannot just be listed in the Malaysian market but internationally as well to get a good range of investors into an initial public offer. If just 20 percent of the shares are offered for sale, the proceeds that the government will get may amount to as much as RM300 billion to RM400 billion, given a P/E range of 15 to 20.

What is Malaysia’s national debt? Official figures put it at RM1.08 trillion with a further RM380 billion guaranteed by the federal government, giving a total figure of RM1.46 trillion. Whichever you take as the debt figure, even RM300 billion will make a huge impact on reducing debt, taking it down to manageable levels.

Short term vs long term

Whether this should be done or not, however, is not so straightforward - there is no free lunch and you can’t create value out of nothing. Since 20 percent of Petronas is no longer with the company, the government will not get as much money as before from it - there will be a 20 percent reduction.

In the longer term, will it benefit the country or will it be better to grit our teeth now and ride the debt and cash flow crisis out by taking concrete steps to stimulate the economy through sustained change over a period of time?

The problem with listing Petronas, although it may improve governance, disclosure, and accountability, is that it offers a quick fix and with all such fixes, there is a tendency towards complacency and increasing government expenditure simply because the capacity to increase it is there.

And yes, there may well be a tendency to try and reward the public too quickly - remember former finance minister Daim Zainuddin’s move through the Council of Eminent Persons to give a six-month reprieve on the sales and services tax even with the removal of the goods and services tax, which would already have crimped revenue?

With Petronas’ profits on an uptrend currently due to increasing energy prices and its cost-rationalisation programme of the last few years, together with the paring of some dubious overseas projects, things are looking up for the national oil corporation.

That also means it will contribute more to government taxes. Together with some other judicious tax measures such as a goods and services tax (it will take some gumption to do this), it does set the stage for a sustainable increase in revenue.

Other measures which the affluent will resist but can easily afford to pay and which have not affected economic performance elsewhere are increasing tax on those earning more money, widening the tax base by lowering personal tax limits, increasing company tax, stopping tax evasion, imposing estate duties and imposing capital gains tax on shares.

To keep on postponing these for political reasons is no longer acceptable. After all, this unity government has a two-thirds majority in Parliament. If enough effort is made to convince all component parties, tough measures can and should be taken.

Leave the golden goose alone, it is still regularly laying golden eggs. Why share these golden eggs forever with others for a one-time payment? There is no good reason right now to sell a stake in Petronas.

P GUNASEGARAM is a former head of equity research and believes that a stitch in time saves nine. He says it’s past time for the government to put in a few stitches right now.

No comments:

Post a Comment